I first speculated that Apple might one day become a bank almost a year before the launch of Apple Pay. What triggered that thought was the use of Touch ID for iTunes purchases and the depth of security involved in the secure enclave used by Apple’s fingerprint system. It was clear even then that Apple had big ambitions in the mobile payment field.

Now that Apple Pay has launched, and already proven a big success, I think the argument for Apple to make the move are even stronger. So here are seven reasons I think Apple may become a bank within the next five years …

1. People hate existing banks

Ok, that’s something of an exaggeration, but not too much of one. It wasn’t like banks topped anyone’s most-loved list even before the banking crisis, but the resulting financial crash put bankers onto pretty much everyone’s hate list. A three-year study of millennials found that all four of the leading U.S. banks were in the ten least-loved brands.

Many people stick with their existing bank for only two reasons: changing banks is a hassle, and they don’t think any other bank would be noticeably better. Those two factors make people look way more loyal to their bank than they really are. Offer them a truly better experience, and a hassle-free way to make the move, and I think many people would switch.

2. People love Apple

Apple’s brand image couldn’t be further removed from that of the average bank. And while Apple’s credentials might not seem to easily translate to banking, there’s one area where Apple’s reputation would mean a great deal: customer service.

Banks are usually dreadful at customer service. They seem to prioritize their own systems and procedures over the customer experience almost every time.

I did actually recently go through the hassle of switching business banks because my old bank not only managed to reject an incoming international payment, it was completely unable to explain why. I logged a complaint, and its complaint-handling was even worse than the original mistake. Mentioning it to friends, this kind of experience appears far from unusual.

Apple’s approach to customer service is up there with the best in the business.

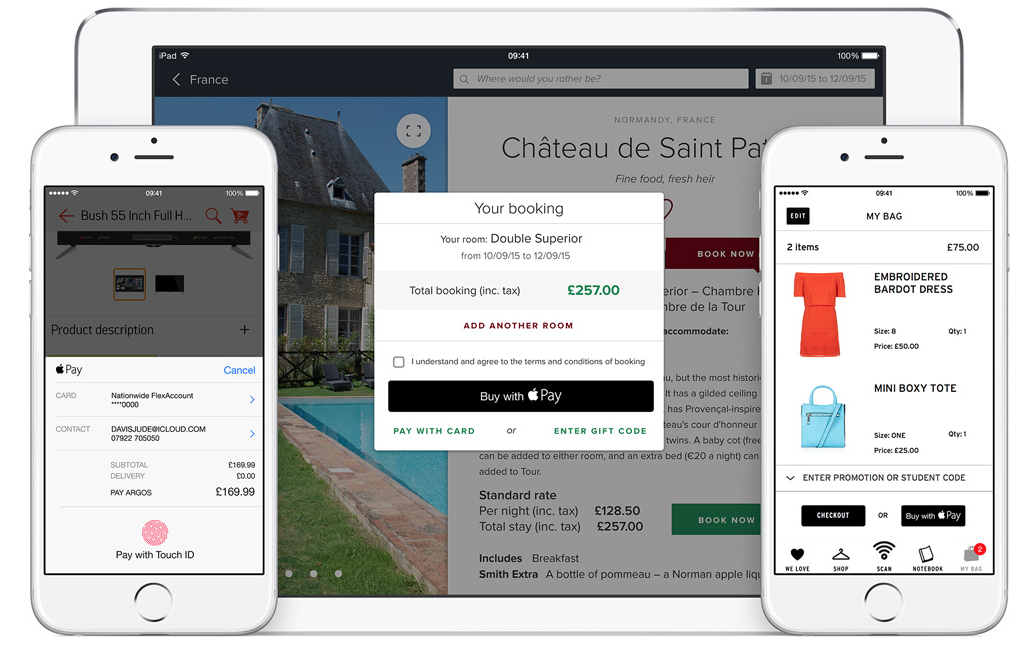

3. Apple is winning mobile payments

Mobile payment was around for many years before Apple Pay, yet adoption in most countries had been extremely low. Apple changed that story almost literally overnight, Tim Cook reporting that the company more than doubled the size of the mobile payment market in just 72 hours, with a million card activations.

Banks have been as keen as consumers to adopt the new payment method, with well over 300 U.S. banks and credit unions now supporting it – and international expansion on the way.

Apple is even effectively acting as a financial gatekeeper, deciding which banks and cards are good enough to be accepted into the program.

4. Apple has the right technology

One of the key reasons Apple Pay has taken off so fast is because Apple Pay offers a greater level of security than any other payment method. It offers the convenience of contactless cards – fantastically convenient but with very few safeguards – with the best security in the business.

The gold standard for card security had, until Apple Pay, been the chip-and-PIN cards used in Europe. Transactions have to be validated by typing in a PIN, with rolling encryption protecting the data stored in the embedded chip. It’s a very secure form of payment – but Apple Pay beats it in two ways.

First, while a PIN should guarantee its the cardholder making the transaction, Touch ID actually does so (low-likelihood hacks aside). Second, while chip-and-PIN hands over your actual card details to the payment terminal, Apple Pay transmits only a one-time code, meaning you don’t have to worry about the retailer’s database being hacked.

5. Apple also knows how to do UI

My bank, unusually, gets a lot of things right. But its mobile banking app is a mess. The user interface is just horrible, and even if I’m logging in on my Mac, I still have to use the iPhone app to generate a code – so I can’t escape that UI.

If there’s one thing Apple (usually!) knows how to get right, it’s the user interface. The right tech working in the right way is going to be appealing right now; factor in a future where banking, like everything else, is going to get more and more hi-tech, and Apple’s UI strength becomes ever more important.

6. Apple has the financial resources

Apple is the largest company in the world. It has enormous cash reserves. Those two facts should make getting the necessary regulatory approvals a done deal, and also lead to extremely high levels of consumer confidence.

7. Younger consumers are ready & waiting

Two recent surveys suggest that millennials – those aged 18-34 – would be more than happy to consider a tech giant like Apple or Google as their bank. The three-year study I linked to above found that 73% would be more excited about a new financial services offering from a large tech company than they would one from their own bank. A separate survey suggests that around half of millennials would specifically be willing to bank with Apple or Google.

Put these reasons together, and I’d put money on it that Apple is at least considering the idea. As with anything Apple considers, that doesn’t mean it will actually do so, of course – and there is one very strong argument against my thesis. For all Apple’s move into services like Apple Music, it is first and foremost still a hardware company. Not only that, but an extremely focused hardware company, famous for saying no to a thousand different ideas for every one time it says yes.

So I don’t think it’s a foregone conclusion. But I do think the arguments for outweigh the arguments against, and that those arguments grow stronger with every new Apple Pay customer. I’m not going to go so far as to say it will happen – but I do think it’s at least a strong possibility.

Am I right, or am I crazy to even think this could happen? Take our poll, and let us know your views in the comments.

FTC: We use income earning auto affiliate links. More.

Apple don’t need to become a bank. I think what they’ll do instead is replace Visa and MasterCard.

hahah “AppleCard”

It’s actually not a bad idea. Like their own credit currency. I can see it like being a way to keep pier to pier credits like venmo.

All things being Apple, I guess the currency could be called ..seeds.

Great article Ben. I’d have to agree with you wholeheartedly. I think it might start with peer to peer payments and expand from there. Lots of regulatory hurdles, but no more than the auto industry. Imagine a “Buy here, ApplePay here! You could order your AppleCar, request a loan, initiate a down payment all from your device and the customized car shows up 2 weeks later. Done and done.

Peer-to-peer could indeed be the next step along the way.

that last sentence, i would love tech like that

The greatest thing against this idea is, in my opinion, all the regulatory problems that it will carry.

Apple likes to be free to change (almost) everything.

And it likes to enter markets that can change. Apple Pay is a big change. What will be the change in banking?

That’s a fair point, but great tech + UI + customer service would represent a pretty big change in itself.

Nice article, Ben. While I don’t think Apple becomes a bank, they might become a payment service provider at a larger scale. Like Visa, MasterCard, or PayPal. Useful features combined with a bank account like Holvi: it combines invoicing and financial reporting and an online shop for small businesses, freelancers, sport clubs … it’s amazing. But they are not a bank, they manage your money in segregated accounts on your behalf. Your money is your money, and managed separate from the company’s funds.

While Apple has no interest in becoming the perfect small business account like Holvi, they might want to become the perfect consumer’s payment service provider: perfect for splitting restaurant bills, sending money via iMessage, paying your landlord via email, paying your energy bill via app and in-app-purchases, even peer to peer loans … and they could make sending money abroad way easier, like TransferWise but at really large scale.

What I’m trying to say is that yo don’t have to become a bank to vastly improve our “banking” experience.

I agree and disagree with you Luis. While Apple does often innovate, it normally just improves upon existing technologies with style. Think about it! The iPhone wasn’t the first touch screen phone, but it was the best. Finger print scanners had been around, but TouchID is better. Mobile payments existed, but ApplePay is taking off because it is better!

And if you are wondering what a BIG change for a bank would look like… Check out Simple. They have already shown how cool a bank CAN be. Here is an interesting read on Simple: http://bit.ly/1N1d2Uv

Maybe a world currency like Bitcoin

I’m all in favor of this. Apple is so huge that if it decided to become a bank, it would definitely qualify to be the first on the list of the banks that are “too big to fail” and thus would always have a guarantee of the taxpayer bailout in case something went wrong. As a shareholder, I would love this.

The reality, of course, is that it will never happen. Apple is extremely cautious about venturing into other areas. I would think that Apple buying Tesla is 50 times more probable than Apple becoming a bank. In fact, I’m surprised that will all of this Apple’s cash sitting in the bank and with the amazing things that Tesla is doing, Apple has not yet acquired Tesla.

The bulk of Apples money is tied up overseas. Bringing it here for an acquisition would incur large tax rates which is why they keep the stock pile where it is. All of Apple’s recent acquisitions have been with loans. I don’t think will shell out the money in the form of a loan to buy Tesla.

I see a lot of reasons why they would make a great bank, I don’t see a lot of reasons what Apple would gain, why they would want to be a bank… What’s to gain for them? (except money, but you know, they can make money by putting a restaurant in the apple stores as well, and they’d probably be great at them and millennial would love it etc; but that doesn’t mean they will…)

8: Banks are going out of business and Apple has all the money.

Absurd, there is always tonnes of bugs update after update and new bugs and security holes keep on coming from almost every updates. So of course no way!

If Apple is smart it will stick with what it does best – electronics. Apple Pay is simply a conduit for people to move money around.The banking business is a different animal.

“Two recent surveys suggest that millennials – those aged 18-34 – would be more than happy to consider a tech giant like Apple or Google as their bank. ”

Well that settles it then, always listen to 18 year olds for good financial advice. Bring on the AppleCare+ for your checks and aluminium debit card.

I think they should totally have pier to pier payments with apple pay. Venmo like functions built into the quick contacts screen of apple watch and spotlight would be awesome.

what about those that don’t have a pier locally or those that are landlocked?

There is much more to banking than the paltry list supplied here.

How about the fact that they might unleash an automobile into the world. Having a bank would be mighty handy as you can control approvals and such.

One minor problem. There’s already an established Apple Bank in the NYC area (with the expected URL). Then again, the Beatles’ Apple label was never successful at keeping Apple out of music.

Apple has always said that they can only do a few things in order to do them great. That’s one of the big differences between them and Google. So, with the “Apple Car” and possibly this banking business… I think the best route to go would be to create subsidiaries or otherwise Apple-held companies that are separate and can fully focus on their products and services, but still integrate with Apple products and fully benefit from Apple’s philosophy, ethics, and company culture. Whether they would consider going that route… who knows.

I don’t see it happening. The level of government scrutiny and regulation that goes with banking isn’t on line wth Apple’s MO. Apple enjoys innovation and free thinking which is difficult to do is such a regulated industry. Plus why become a bank when you can stronga a bank and shave a little off the top. Take the burden of liability off of Apple and onto the banks and make more profit with something consumers want. Same applies for credit card companies. Why get into the industry when you can make the industry do what you want and remove liability.

Apple’s become a payment processor, but that’s a far cry from being a bank. Payment processing, for Apple, is a way of keeping people tied to their platform (and I mean that in a “good for business” sense, not in a negative way). Just as Apple gives away their software to make their hardware more compelling, payment processing is another value-add that puts them into a dominant position and fends off competition. But there’s no reason for them to become a bank – and given the massive amount of regulation on banks, there are plenty of reasons NOT to. And look at what banks make in profits these days – fractional percentages. Unless you get into investing, there’s simply not much profit in being a bank. *Facilitating* financial transactions, sure – that’s always been a bigger money-maker. But that’s not the same as being a bank.

I’ll point out that everyone, forever, thought that Apple’s play into payment processing would involve their millions of iTunes accounts – and it didn’t. It’s just your same old credit card, being handled in a new way.

And there’s some naïveté, here – Apple might be “winning” mobile payments, but mobile payments isn’t “winning” anything. It’s a fraction of a fraction of payments, and despite the millions of card activations, consumers still aren’t consistently using their phone or watch to pay. Online payments are a much bigger deal than in-person, in terms of growth potential, and Apple hasn’t made any moves to process those transactions differently. What Apple is doing is great, and it’ll hopefully grow into something wonderful, but it’s leagues away from them being a bank and actually holding people’s funds, issuing loans, investing money, and so on.

Could Apple improve the mobile banking experience? Sure, but they don’t need to *be* a bank to do that, any more than they needed to be a bank to create Apple Pay. Apple could certainly do a lot to improve banking, but opining that they should or could *become* a bank unfortunately suggests you don’t know a lot about the subject. In reality, nothing Apple has done really qualifies them to become an actual bank.

Addressing the latter first, Apple is in a position to buy in all the expertise required – much as it did (on a smaller scale, obviously) with watches.

Similarly, mobile payments are small now, but will grow very rapidly indeed. Within ten years, nobody in the USA or Western Europe is going to be using slices of plastic to make payments.

The profit argument is a reasonable one, but you could have said the same about the smartphone industry prior to Apple …

It’s will take a lot longer than ten years for that to come true. There will be many very small stores and restaurants that will not be on the system. I think fifteen years is more likely, it will be much longer before the rest of the world gets totally on board, if ever. Many areas can’t even afford a bank account for credit cards.

https://squareup.com/apple-pay

Card issuers are also not banks. Apple could realize some decent profits as a credit issuer, but even that seems unlikely. More likely would be something like PayPal, which is a processor that also holds balances (one small aspect of what constitutes a bank).

Investing is something Apple is already doing and they don’t need to become a bank to continue. It just looks like a mountain of effort to make a mole-hill of profit. Unless of course we change the definition of “bank” to be something it isn’t. ;)

Bruno + 1000

I could see Apple buying Square, but what will Apple do with it once they bought them? For Apple, it has to be related to their product line, like Apple Pay. There has been no indication of Apple driving their product line in any way toward taking payment for anything else but their own stuff. Like others have have said, I couldn’t see Tim Cook willing to go through the regulatory hurdles and tie their business to anything requiring that much government regulation.

If Apple wanted to ever get in to the banking business of any kind, the product they would release along with it would be the biggest thing ever launched by any company anywhere and at any time. It would have to be bigger then what J.P. Morgan did for the U.S. financial system.

Five things I would like Apple to become in the future: wireless company, proper camera brand, car maker, bank, university.

University, yeah! That would be a dream come true.

I’ve always wondered why Apple has never gotten into cameras (well they sort of did years ago) and wish they would.

As Apple states, they are the world’s largest camera company. Whi,e you’re thinking about standalone cameras, Apple isn’t interested in that.

If we get a real optical zoom built in, then the demise of the compact camera is near. As it is, sales in all camera categories, except in mirrorless, which isn’t going anywhere right now, is falling, compact cameras are being hit the worst.

I rarely carry my big DSLR with me any more.

To be fair they aren’t really. Samsung has a lot more phones in the wild with cameras, so Apple saying that is just marketing speak.

You are right though, compact cameras will be hit the worst I think.

They may be the biggest business in the world, but Banks have more clout in the financial world.

Apple needed the cooperation of Banks to make Apple Pay successful in the first place, the Banks could just as easily refused to accept it, and it’s not too late for them to turn against the format. I don’t think Apple would have got that cooperation without agreeing to stay out of the banking business.

Extremely not likely. Everyone keeps thinking Apple is this giant company but they’re not realistically, in terms of non-retail heads, they’re fairly small around 20-30K and the amount they need to handle all the legal stuff in each state and federal laws would cause them to triple it and Apple does not scale well. There’s a reason their QA keeps going down every time they expand a new project.

If anything, Apple is likely to launch a virtual service on top of existing banks like Simple. Think Apple Pay but extended to cover savings, checking, and so on.

I would rather Apple use credit unions instead of banks, that would really rock and hurt banks far more than Apple doing its own bank.

I think they will look long and hard at this, but the biggest reason for them that i see is not the customer side of the business, it would be the investment and movement of money (and huge sums of it) from continent to continent. They could effectively lend what they have overseas to a business in the USA and use the money rather than just having the money…! They also have the structure and security for banks to already be available in pretty much every major town now as well, so a financial centre in store is not such a huge move from being just a store…

This article is totally forgetting that banks make almost no money. It would be a huge loss leader for Apple, and to what end?

The PC industry makes almost no money; ditto the smartphone and tablet industries; and Spotify hasn’t made a single penny in profit. That other companies haven’t found a way to make something profitable doesn’t necessarily mean that Apple won’t …

Being the richest and most profitable business in the world doesn’t make Apple immune, God-like or above the law. They are still subject to market forces & government regulations like every other business.

Not everything they touch turns to gold. The jury is out on the Apple Watch (though I love mine). The Macintosh has been out for a quarter of a century and has less than 10% of the PC market. The iPhone, iPod, iPad & Macbook lines are huge successes yet the Apple TV could be classed as a failure. Apple Pay has been available for coming upto a year and is still only available in the US at a handful of retail stores.

I think Bruno has said above that something along the lines of Paypal may be a plan and I agree with him. It’s probably a lot less complicated to regulate and maintain :)

Apple Pay is currently held back by the fact that the USA only recently adopted contactless payment; in Europe, contactless has been used for years and is everywhere. The same thing will happen in the USA, I’m sure.

Just because Contactless has been prolific in Europe for the last couple of years, doesn’t mean it doesn’t still have its glitches. There are many stories of people being charged twice for the same purchase because they opted to use a regular payment method and held their purse – with contactless card in it – too near to the terminal, which proceeded to charge them a second time. It still happens too, so it’s not the perfect technology just yet.

No technology is perfect, indeed (though personally the only thing I’ve ever had happen when accidentally presenting two cards is that payment fails).

If they do, it would be PayPal style. I can’t see them becoming a traditional bank. I could definitely see them wanting to take over the user experience for other banks with a built-in finance app that complements Apple Pay though.

I guess we’ll find out eventually if they want to venture into this arena but I think another indicator that they’re at the very least considering it is their recent PR focus on privacy and security of their products and services.

Apple could replace a lot of banks but it could never replace a Military bank. Because we get better benifits.

How much would they charge users to facilitate banking with them? 30%? LOL

Anything branded Apple creates confidence with consumers. That’s a huge selling point for the retailer in that they use Apples hardware and back end which drives their sales up (remember iBeacons? It’s such a lovely shopping experience at the Apple Store), it drives Apples hardware up because people will want to use this service, and Apple skims a little off the top. They do all of this without being a bank or a credit card company.

I see this trend growing. With jack Dorsey going back to be the Twitter CEO and Apple calling out Square by name at WWDC. I think an Apple buyout of Square is highly likely. The issue Apple has no is that they have one end of the spectrum (the end user) but not the retailer (which they are trying to do with iBeacons) imagine adding a POS system into it which is simple and integrates with an iMac. Add in an API so Apple can force someone like Quicken with Quickbooks to go through the Mac Apple Store (any Apple gets their 30%) and all the POS transaction and back room stock info are all these for you. It’s such a win. I think this is what Apple will do instead of going the route of bank or CC company. Too much hassle when they can strong arm these companies into letting Apple take a slice without it affecting the end user.

All your arguments are rock solid but there’s one big reason why this will never happen: Apple isn’t interested in becoming a bank. Apple has become really successful because of one thing only: razor sharp focus. While that was even more the case when Steve was still around Apple is still very careful which markets it enters. Banking is a whole different business that isn’t like any other business. It will mean Apple needs to take risks with money and a service that can be very profitable when done right but also can get you bankrupt in no time when executed poorly.

Apple Pay was introduced to be a great feature for the new iPhone and Apple Watch. Sure there is more to it. But for now Apple is focussed to make their existing hardware more useful.

What are they going to cal it?

https://www.applebank.com

Nordstom is a bank, and they have less money XD

Need another poll option: i wish but it will never happen.

Unfortunately the regulatory requirements you mentioned in passing may become a huge issue. I don’t see the government allowing the leap to becoming a bank.

The kinds of services (loans, mortgages, fee accounts) that make a bank profitable involve much more than superior Tech + UI + Customer service, and even then the investment wouldn’t yield as much margin as shareholders are used to. They might go as far as competing on P2P payments a la Venmo, but not much further than that.

They will have all my money.

I can give one reason: Apple Pay

Step one would probably be to launch a “Snapcash Killer” to make it super-easy and super-fast to transfer money from one Apple Pay member to another. Super-easy way to pay for rounds, split bills etc. It obviously exists today, both from banks and from Snapchat, but Apple doing it could really make it mainstream. Solidity and trust of a bank, technical knowledge and number of users like Snapchat.

Apple already controls a lot of the money flowing through it – why take on the burden of regulation, with little upside to show for it?

Also, banking generally has much lower profit margin than Apple’s current level, so it wouldn’t be a great addition anyway.

Also, the issue with bank is not that people hate it (generally they don’t it’s just the loud minority you hear all the time) – most people don’t care about banking (not just banks) at all.

I’d written about this topic this year on my blog on FinTech (theFinTechBlog.com). Citi had proposed doing the behind the scenes work (back office etc.), so that Apple could launch Apple Bank with its brand and superior user experience. Eddy Cue took idea to senior leadership, then came back to tell Citi, after much discussion, the team felt “Apple isn’t a $%*!’ing bank.” :-) Here’s a link to the post on Apple > http://wp.me/p5glqp-4R.

I first thought Apple would become a bank in 2010, when I was receiving payments for App Sales.

How easy the transition would be to allow me to store up revenue earned from app sales and then buy stocks with Apple’s existing stock app or even other Apple products.

Look at Paypal, bitcoin to see the disruption in banking, Apple doesn’t even need to have a bricks and mortar infrastructure for this- it just needs your Apple ID. Credit and ‘money’ is now all bits and bytes linked to an individual or a business identity. For business banking, Apple’s very thorough in confirming a corporation’s physical address and corporate records for the Developer Program- so they’re collecting revenue from sales, how much extra work is it to allow those revenues to be held and/or accumulate interest?

Now, let’s look at insurance and how Apple’s Health Kit will be linked to an insurance policy? Apple knows from the motion chip- M7 and M8 of every individual iPhone how healthy you are. And of course Apple Watch can monitor health and healthy choices even more closely, why not use the infrastructure of collecting payments for insurance premiums? Having worked for the 3 largest insurance companies in Canada- every insurance and banking employee can be replaced by code.

The reasons listed are why Apple could become a bank, but I don’t see a reason why Apple would want to become a bank? What do they gain by being a heavily regulated commercial institution?

The one and only reason they won’t… It’s illegal in the U.S. Walmart tried to form a bank so the U.S. outlawed it. Apple would face a similar issue in its home market.

http://www.wsj.com/articles/SB116118495912296504

My reading of that piece is that it doesn’t say it’s illegal, but rather says that legislators want to make one route to becoming a bank – ILCs – more difficult.